Taiwan Semiconductor Q3 2024: $23.5B Revenue, 36% YoY Growth, and Record $10.06B Profit

TSMC reported impressive results for the third quarter! Their revenue hit NT$759.7 billion, which is the highest ever and shows a 39% increase compared to last year. Their net profit jumped to NT$325.3 billion, raising earnings per share to NT$12.54, a 54.2% increase. The gross margin was an excellent 57.8%, higher than the expected range […]

TSMC reported impressive results for the third quarter! Their revenue hit NT$759.7 billion, which is the highest ever and shows a 39% increase compared to last year. Their net profit jumped to NT$325.3 billion, raising earnings per share to NT$12.54, a 54.2% increase. The gross margin was an excellent 57.8%, higher than the expected range of 53.5%-55.5%, and the operating margin reached 47.5%, exceeding the guidance of 42.5%-44.5%.

Taiwan Semiconductor Q3 2024 Earnings Summary

Revenue: $23.5 billion (estimated $23.3 billion); up 36% from last year

Gross Margin: 57.8% (estimated 55%); up from 54.3% last year

Operating Margin: 47.5% (estimated 44%)

Net Profit: NT$325.26 billion ($10.06 billion); the highest ever

Q4 2024 Guidance:

Revenue: Expected between $26.1 billion and $26.9 billion (estimated $24.94 billion)

Gross Margin: Expected between 57% and 59% (estimated 54.7%)

Operating Margin: Expected between 46.5% and 48.5% (estimated 44.3%)

Full Year 2024 Outlook:

Revenue Growth: Close to 30% (up from mid-20%)

Capital Expenditure: Slightly over $30 billion (estimated $30-32 billion)

AI Processor Revenue: Expected to triple, making up a mid-teens percentage of total revenue

Segments:

Wafer Shipments: 3.338 million units; up 15% from last year

Average Selling Price per Wafer: $6,131; up 18% from last year

Advanced Technologies (7nm and smaller): 69% of wafer revenue

3nm: 20% of revenue (up from 15% in Q2)

5nm: 32% of revenue (down from 35% in Q2)

7nm: 17% of revenue (unchanged from Q2)

Product Revenue:

High-Performance Computing: 51% of total revenue

Smartphones: 34% of total revenue

Combined (HPC + Smartphones): 85% of total revenue

IOT: 7%

Automotive: 5%

Data Center: 1%

Others: 2%

Revenue by Region:

North America: 71%

China: 11%

Asia Pacific: 10%

Japan: 5%

EMEA: 3%

Operational Highlights:

3nm Technology: 20% of total wafer revenue, performing better than the previous 5nm ramp-up by 30%

Utilization Rates: Increasing due to strong demand for AI

Capital Expenditure: $6.4 billion in Q3; 2025 capital spending expected to be higher than 2024

Expansion Plans:

Arizona Factories: Production expected to start in 2025

Japan Factories: First factory will start production this quarter; second will be operational by 2027

Europe Factory: Production expected by 2027

CEO C.C. Wei’s Comments:

The demand for semiconductors is very high and is just beginning.

They are seeing strong AI-related demand, which is increasing capacity utilization for their 3nm and 5nm technologies.

High gross margins are crucial for sustainable growth in their capital-intensive business.

They expect healthy growth next year and higher spending in 2025.

AI revenue growth is likely to boost long-term growth, but no specific numbers were provided.

Additional Insights:

Intel remains an important customer with significant contributions.

Demand for advanced packaging (CoWoS) is greater than supply, with plans to double capacity by 2025.

Non-wafer revenue now makes up over 10% of total revenue.

Challenges Affecting Gross Margin:

New overseas factories may reduce margins by 2-3% each year.

The ramp-up of 3nm technology could cause a 3-4% reduction.

Converting from 5nm to 3nm will reduce margins by 1-2%.

Inflation, exchange rate changes, and rising electricity costs are also expected to impact gross margins in the coming years.

Related News

Ola Electric Layoffs 2026: Company Cuts 5% Workforce, Expands Automation for Profitability

MNRE Confirms No Advisory to Stop Renewable Energy Financing

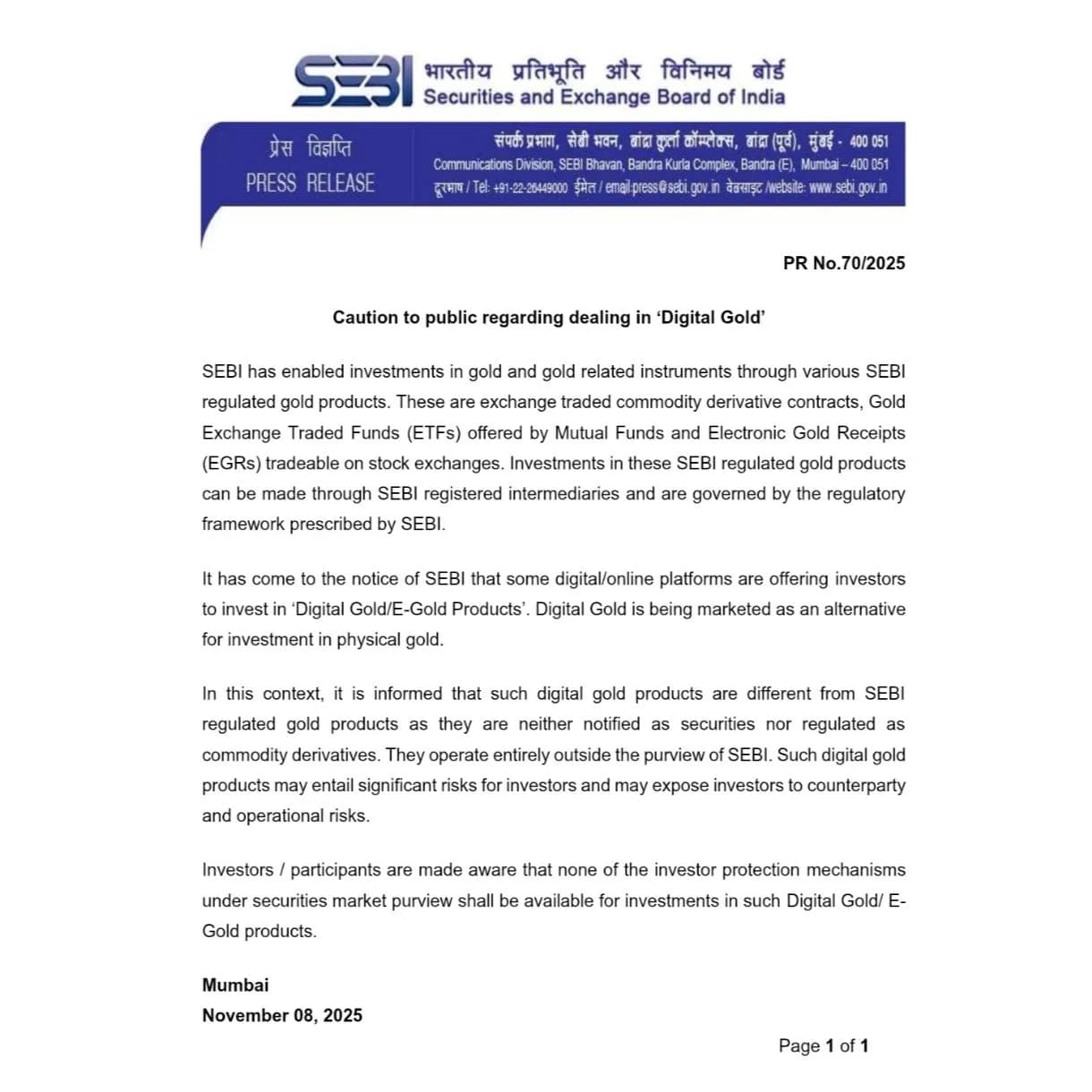

SEBI Warns Public Against Unregulated Digital Gold Investments

India Manufacturing PMI September 2025 Shows Slowest Growth in Four Months

LIC Reduces Stakes in 81 Companies, Adds Defence Stocks in Rs 15.5 Lakh Crore Portfolio Reshuffle